Today, Royal Den Hartogh Logistics, specializing in global transportation for the chemical, gas, and food industries, announced an expansion of its portfolio through the acquisition of H&S Group, which is active in transporting liquid foodstuffs in Europe. The French company Stef Groupe increasingly relies on revenue and results growth from international activities in North European contract logistics following the acquisition of Bakker Logistiek and Transwest last year. Recently, there was the acquisition of Bollore by CMA CGM or Scan Global Logistics by CVC.

Further M&A consolidation

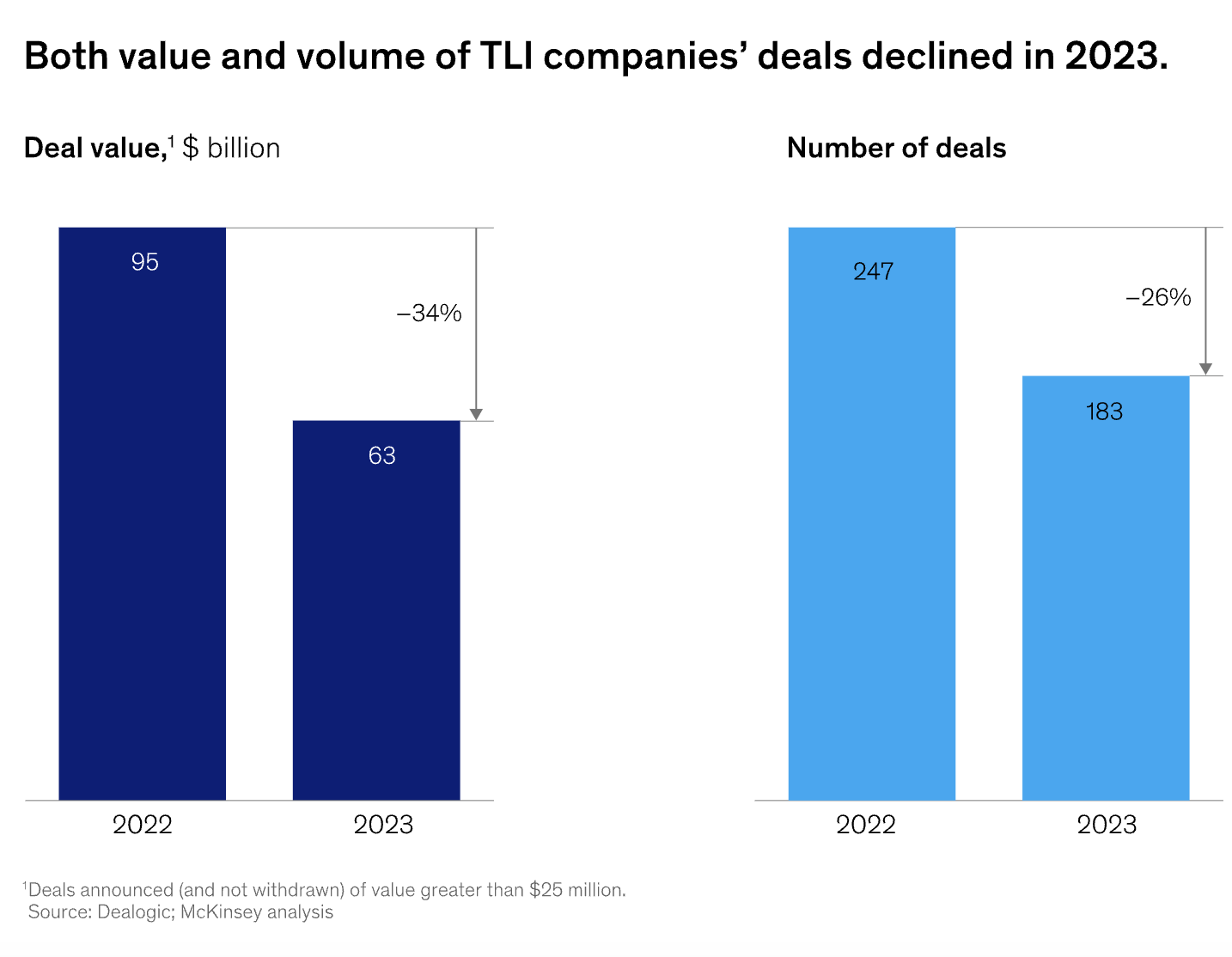

MCF Corporate Finance, a principal German advisor in international acquisitions, forecasted the logistics market to experience further M&A consolidation driven by large cash reserves of maritime shipping companies and increasing awareness of logistics as a critical value differentiator, making the industry attractive for financial investors. McKinsey says that the pandemic-fueled rout in 2020 to 2021’s record-breaking recovery, followed by a steep decline in 2023, the global M&A market has offered something of a masterclass in volatility.

Source: McKinsey

Increased interest rates, declining freight rates, and geopolitical uncertainties have significantly impacted the M&A dynamics, leading to a decline in M&A activity for operating logistic companies.

Despite the significant geopolitical risks for global trade, including potential conflict escalation in the Middle East, pivotal elections in the US, India, and the European Union, and ongoing economic challenges in China, MCF anticipates a more promising year for M&A in 2024. The logistics market continues to boast record levels of liquidity, which will likely be directed towards share buybacks or M&A activities. Moreover, the impending sale of DB Schenker will profoundly influence market dynamics, while private equity firms hold substantial dry powder ready for investment. The MCF report elaborates that the market landscape presents opportunities for sellers and buyers.

Stability in valuation levels

The valuation environment for logistics companies has remained stable, and its current valuation level is in line with the historical average, trading at approx. 9.7 x EBITDA), according to MCF. The valuations for historical transactions have remained in line with expectations. For transactions exceeding a valuation level of euro 100 mln to euro 1 bln, MCF observes valuations between 6.5 – 8.5 x EBITDA as the industry average. Whether the upper or lower end of this range is met depends significantly on the end markets of the customers, the company’s infrastructure base, and the proof of growth in recent years. Valuations can substantially exceed the abovementioned range in case synergies are priced in – often in well-structured M&A processes. MCF observes multiples of more than 10x EBITDA (and by that, in line with public valuation levels) for transactions with an enterprise value of more than euro one bln valuations.

Major forces transforming the transport industry

Dealmaking in 2024 and beyond must take into account major forces that are transforming transportation and logistics, according to McKinsey:

- Financial forces: 2024 looks attractive for buyers. From 2020 to 2022, logistics players accumulated deep cash reserves that they had to tap in 2023. Now, they face a new financial reality with the rising cost of money. Many logistics companies will have difficulty securing financing. Many would-be sellers will also find limited demand for their assets. McKinsey does not expect demand to rebound to pandemic levels. Demand stabilizing at 2023 levels will push valuations down and force less competitive players to rethink their business plans.

- Market forces: The transportation and logistics sector is growing more complex and competitive. Only the financially fittest will survive. Shippers’ demand for more services and visibility is pushing logistics players to invest in broader, more diversified service portfolios, vertically integrated services, and intermodal solutions. Meeting these requirements translates into more complex supply chain designs with greater speed, broader geographic coverage, and more cost-competitive offerings. Emerging expectations for sustainable operations will complicate the picture. While feeling mounting pressure to deliver more, logistics players must often do so with less. Churn, especially among truck drivers, is a severe problem that has profound implications for operating and recruiting costs, not to mention service quality.

- Technology forces: Leading-edge supply chain designs will fully exploit advanced digital capabilities and automation in sales and operations, from building online channels to conducting deep analyses of the supply chain network to identifying commercial opportunities. Artificial intelligence, from analytics to electric vehicles to warehouse robots, will play a key role.

The growing significance of technology is tilting the scales in favor of top strategic and financial investors in 2024 and beyond. With substantial financial resources, they are well-positioned to acquire digital capabilities, thereby gaining a formidable competitive edge. Companies unable to match this pace may find it beneficial to explore acquisition opportunities, enabling them to access capabilities that would otherwise be financially out of reach.

Opportunities

Amidst the challenging macroeconomic landscape, there is an opportunity to enter or expand market share at comparatively lower valuation levels in the private sector. This is likely to spur an uptick in M&A activity rather than share buybacks, particularly given the historically high valuations in the stock exchange. Nevertheless, assets with compelling equity narratives are expected to command premium valuations despite their scarcity.

MCF sees three primary strategic drivers for M&A activity:

- Integration of services: sea and air freight entities enhance their value chain capabilities by bolstering their road capabilities.

- Strengthen market presence: American and Asian firms seek to strengthen their presence in Europe, particularly in the UK, Benelux, and Germany.

- Investment opportunities: private equity firms consolidate the market across diverse services and geographical regions to create comprehensive one-stop-shop solutions.

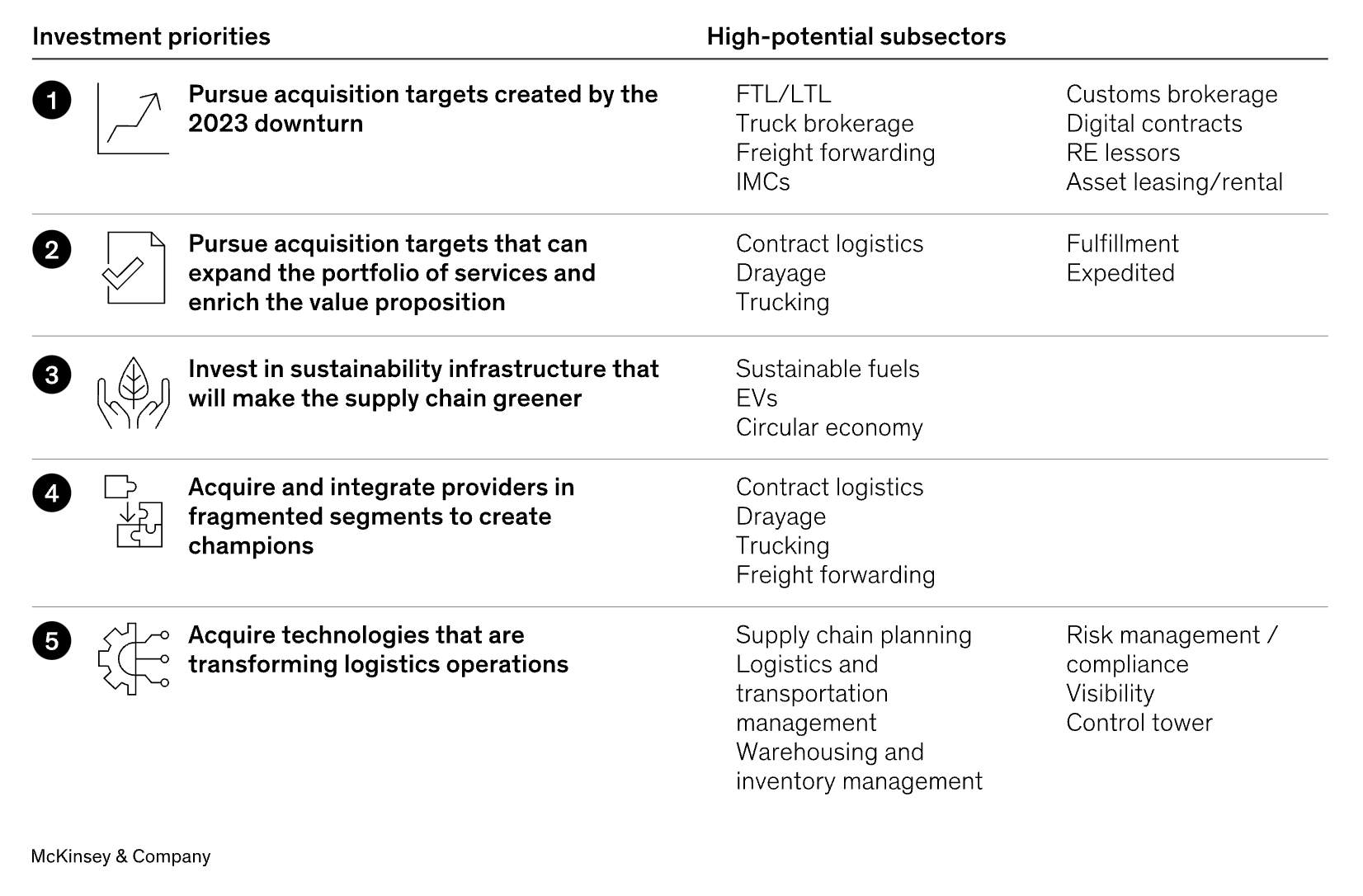

McKinsey sees five opportunities for buyers:

- Opportunistically pursue acquisition targets created by the 2023 downturn. Many midsized companies in various segments fit the bill for the right value.

- Pursue acquisition targets that can expand the portfolio of services and enrich the value proposition. These will often be viable businesses in market segments that other companies ignore or businesses with assets that would be difficult to replicate.

- Invest in sustainability infrastructure that will make the supply chain greener, pleasing shippers and the government. Opportunities here range widely, from cleaner fuels to electric vehicles to circularity.

- Acquire and integrate providers in fragmented segments to create champions. The top ten providers in a segment like contract logistics represent only about 5 percent of the market. Hence, investors, especially leading financial investors, stand to profit from buying several companies at attractive prices and rolling them up into a single company that has a broader geographic reach and a more extensive customer base.

- Acquire technologies that are transforming logistics operations, mainly digital and automation capabilities. Appropriate targets will be companies that have or are developing these technological capabilities.

Sources: MCG and McKinsey